Executor Liability: Can You Be Held Personally Liable?

Being asked to act as an executor is a real mark of trust, but the executor role brings legal duties that many people do not expect. One worry we hear often is whether you can end up out of pocket if something goes wrong. The honest answer is that an executor can be held personally liable in certain situations, though with care and the right guidance the risk stays small.

This guide explains when executor liability arises in the UK, how long it lasts, and the reasonable steps that keep you protected.

Can an executor be held personally liable?

You might be asking, can an executor be held personally liable? Yes, but executor liability arises only where they have fallen short of their legal duties. An executor who acts honestly, follows the correct process and takes professional advice has very little to fear. You are only personally responsible where a loss results from your own fault. Acting in the best interests of the beneficiaries, rather than for any personal gain, keeps you firmly on the right side of the line.

Understanding executor liability in the UK

Executor liability means being held legally responsible, out of your own funds, for a loss the estate suffers because of something you did or failed to do. In law this is sometimes called a devastavit, which means wasting the estate. If beneficiaries or creditors lose out, they can ask you to make good the shortfall yourself, which is why many executors take professional legal advice early. Some of these terms are explained in our plain English glossary of probate terms.

What does an executor actually have to do?

Before any question of liability arises, it helps to know what the job involves. As the named executor in a valid will, you are legally responsible for the deceased's estate. Your first task is usually to register the death, obtain the death certificate, and apply to the Probate Registry for the legal authority to act. Without that legal permission, financial institutions will not release the money, property and possessions held in the deceased's name.

Once probate is granted, you gather in everything the deceased owned. That means contacting banks, building society accounts, pension providers, utility companies and other relevant organisations to close accounts and settle balances. You may need to work out the estate value, sell property, collect any rental income, and follow the deceased's funeral wishes, paying the funeral expenses and other funeral costs from what the deceased left before distributing assets to the beneficiaries.

When is an executor personally liable?

Most claims against executors trace back to a handful of common mistakes. Knowing them in advance is the surest way to avoid them.

- Paying out too early and not keeping enough money back to cover a later debt or claim.

- Distributing the estate to the wrong people, or overlooking a beneficiary such as a surviving spouse or civil partner.

- Getting the inheritance tax forms wrong, or paying the tax late and running up interest and penalties.

- Failing to settle outstanding debts and taxes before sharing out what is left.

- Losing or mismanaging financial assets and property, such as letting a house fall into disrepair.

There is also a right order in which to pay what the estate owes. Estate liabilities, including any outstanding debts, must be paid in a specific legal order, and where an estate is insolvent and cannot cover everything, the law dictates a strict order of priority for creditors. Paying debts in the wrong order, or paying a beneficiary ahead of a higher-ranking creditor, is one of the clearest ways to face executor liability. Can you protect yourself against debts you do not know about? Yes. Executors can place statutory notices to protect against unknown creditors, and a notice gives creditors at least two months to come forward before you distribute.

In each case the problem is not bad luck but a failure to follow the proper process. If you feel out of your depth, our team can handle the whole probate and estate administration for you on a fixed fee, so the responsibility does not rest on your shoulders alone.

How long can an executor be held liable?

There is no single cut-off date, which surprises many people. You may have heard of the executor's year, the idea that an estate should be wound up within twelve months of the death. That is only a guide, not a deadline, and executor liability can continue beyond it. A common question is how long to wait before paying the beneficiaries. As a rule, executors should wait at least six months after the probate before distributing funds, which leaves room for any late claims against the estate.

Some claims carry their own time limits. A claim under the Inheritance (Provision for Family and Dependants) Act 1975, for example, must usually be brought within six months of probate being granted. Once you are granted probate, the clock starts on several of these limits, so keeping accurate records throughout the administration period protects you if anyone questions your decisions later on.

The main time limits to keep in view are set out below.

| Situation | Time limit | Why it matters |

|---|---|---|

| Winding up the estate (the executor's year) | A guide of around twelve months, not a fixed deadline | Sets a reasonable pace; liability can continue beyond it |

| Claim under the Inheritance (Provision for Family and Dependants) Act 1975 | Usually within six months of the of probate | A late claim can still affect how the estate is shared out |

| Paying inheritance tax | Generally within six months of the end of the month of death | Interest, and then penalties, build once the due date passes |

How to protect yourself from personal liability

Managing executor liability comes down to a few sensible steps that any executor can take.

- Place statutory notices for creditors under the Trustee Act 1925, advertising in The Gazette and a local newspaper, then wait the required period before distributing.

- Obtain professional valuations for property and other significant assets.

- Settle all debts, taxes and inheritance tax before paying any beneficiaries.

- Keep detailed estate accounts and a written record of every decision.

- Take advice early, especially on tax and anything that looks complicated.

These steps reduce your risk and give the beneficiaries confidence that the estate is in safe hands. Making a clear, up-to-date will also makes life far easier for whoever takes on the role.

The executor and inheritance tax

Tax is one of the biggest areas of legal responsibility for an executor, and one of the easiest to get wrong. As well as inheritance tax, there can be income tax on any earnings up to the date of death. There can also be capital gains tax if assets are sold for more than they were worth when the person died. You report and settle these with HM Revenue and Customs, and errors here are a common source of executor liability.

When is inheritance tax due? It is generally due within six months of the end of the month of death. In most cases the tax, or at least the part not being paid in instalments, has to be settled before the probate can be issued, so it is worth dealing with tax matters early. Tax is also one of the easiest parts to hand over. If you would rather not deal with HMRC yourself, talk to our team about handling the tax matters on a fixed fee, so nothing is missed and no deadline catches you out.

Frequently asked questions

Can an executor access the deceased's bank account?

Not straight away. Banks usually freeze the account on death and release estate funds only once they see the grant of probate, although most will pay direct costs like the funeral first. Each bank sets its own limit for releasing money without a grant.

Are co-executors liable for each other's mistakes?

They can be. Where there is more than one executor, they are usually held jointly responsible for the estate, so it pays to stay involved and informed even if one person handles most of the day-to-day work.

Can an executor refuse the role?

Yes, as long as you have not already started dealing with the estate, which is known as intermeddling. You can formally renounce the role or step back before taking it on, and someone else can act instead.

How do you get probate?

You apply to the Probate Registry, and the grant confirms the will's validity and your authority to act as executor.

Does executor liability insurance help with unknown creditors?

It can. The cover may pay out on certain claims, such as a missing creditor or an unknown beneficiary appearing after the estate has been shared out. It gives extra peace of mind on larger or more complicated estates.

Worried about getting it wrong? We can help

You should never feel pushed into taking on more than you are comfortable with. From our base in Ware, Hertfordshire, we guide executors across the county through probate with fixed, transparent fees. We can take on as much or as little as you need, from obtaining the grant of probate to handling the full estate administration.

Whether you simply want to check you are on the right track, or you would like the whole job taken off your hands, talk to us first. To find out how we can help, visit The Probate Bureau or get in touch with our friendly team today. We will explain your options and exactly what it will cost, with no pressure.

Back To BlogShare This Post

Recent posts

- What Are the Duties of an Executor? By , 15/06/2026

- Executor vs Administrator UK: What’s the Difference? By , 15/06/2026

- Executor Liability: Can You Be Held Personally Liable? By , 15/06/2026

2015 Archive

2016 Archive

2018 Archive

2019 Archive

2020 Archive

2023 Archive

- July 10 posts

0 Archive

- December 1 posts

Blog Categories

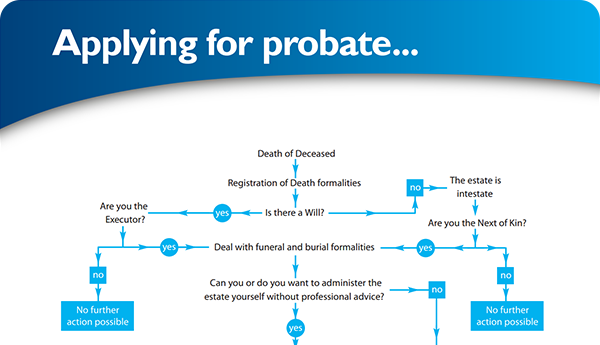

Find your way through the probate maze

Click here to follow our step-by–step probate process guide

Testimonials

Excellent service, everything went very smoothly. Like to thank Ann and her team.... read more

Good & Reliable service, always kept up to date with what was happening. Value for money.... read more

Latest Tweet

Follow @ProbateBureau

Contact Us

0800 028 2837 info@probatebureau.comTHE PROBATE BUREAU

3 Crane Mead Business Park

Crane Mead

Ware

Hertfordshire

SG12 9PZ

×